Not surprisingly, the devil is in the details.

www.istockphoto.com

Most of the things we spend money on combine two elements that determine their pricing or worth: the utilitarian and the subjective. While a refrigerator is more useful than a masterpiece painting, it holds a much lower market value. One is practical and common, the other is aesthetical and unique. Once any society has enough material goods to meet its basic needs, it starts to create (and assign value to) things that have no utilitarian purpose. The entire art industry, for example, exists only because a consensus of people decides that this painting or that sculpture is aesthetically valuable…and therefore it is valuable. Every so often, the perceived value of a particular product triggers a trend, which can explode into a collective “mania.”

An NFT, which is short for Non-Fungible Token, simply enables people to go crazy over a non-physical thing.

Spoiler alert: This may be the only “simple” idea in the pages that follow.

A year ago, I penned a feature for EDGE that attempted to explain cryptocurrencies in general, and Bitcoin in particular. The assignment was to make the article informative and entertaining. I am told the story received very positive feedback from readers who wanted a rudimentary explanation of them from someone who started with a rudimentary understanding of the topic. From that rudimentary understanding, my personal conclusion was that—owing to my wariness of the underlying fundamentals and my suspicion of all the hype—it was not for me. Since then, despite the best efforts of Larry David, Matt Damon, and other celebs who hopped aboard the crypto train, the dollar values of many cryptocurrencies, including Bitcoin, have plummeted by two-thirds or more.

In that story, I did not mention Ethereum, a second major player in the business, which is similar to—but not a carbon copy of—Bitcoin. Ethereum operates on a newer form of blockchain that has set off the latest round of speculative bedlam by introducing to the crypto universe a “digital asset” called an NFT. I wasn’t exactly shocked when EDGE called and asked me to take a shot at explaining NFTs to the magazine’s readers.

So what is an NFT? First off, let me say that I’m neither the first person nor the last to attempt a brief, simple yet coherent answer to this question. Let me also say that, in a world saturated with mis-, dis- and mal-information, much of what I encountered online while researching and writing this story was problematic—and in the case of one NY-Metro newspaper, mostly wrong.

Let me take you back to where I started: the drawing board. While I do, however, keep in mind something Ayn Rand once said: “Greed is the desire for the unearned.”

NFT By the Letters

www.istockphoto.com

Let’s start with the F in NFT: fungible. It’s an adjective with a textbook definition: “Of goods contracted for without an individual item being specified, replaceable by an identical item…or mutually interchangeable.” A bag of salt is fungible. If you want one, any one will do. Picasso’s Guernica? There is only one. This is where the N in NFT comes into play. Guernica is non-fungible. Non-fungible things tend to be more valuable than fungible ones.

Can a fungible item “become” non-fungible? Indeed it can. Think of an 8 x 10 publicity photograph of Tom Cruise, which might be printed in the hundreds or thousands. These are fungible. However, once Tom signs one of these photos, that single autographed print is technically unique and non-fungible—although you could argue that one Cruise scrawl is no different than another. Nonetheless, it would certainly be more valuable.

Now let’s talk about the T in NFT. It stands for Token, though not the kind you used to use on the subway or move around a Monopoly board. In this context, a token is a unit of value that is recorded as a receipt on something called a blockchain; if you’ve heard of NFTs or cryptocurrency, you’ve no doubt encountered this word. The people who use it toss it around as if everyone else obviously knows what it means…which is not the case…because it’s incredibly complicated. I offered an explanation of the blockchain in my cryptocurrency story last year and I think I’ve gotten a bit better at it since then. Here goes:

Let’s say that you want to buy a pair of shoes from Bob’s Boutique, which charges you $100. You don’t have cash, so you insert your debit card. The terminal sends a message to your bank that says I have an account with you and want to spend $100 at Bob’s Boutique… please send $100 to Bob’s bank. This is the meat and potatoes of what banks do millions and millions of times all day, every day, meticulously recording every transaction. At the end of each day, they tally up all the transactions and settle the accounts; your account balance is reduced by $100 and Bob’s is increased by $100. We trust our banks to keep perfect records, which is why we call them fiduciaries. It’s a system that’s been around since Renaissance Italy, and it works pretty well. With the advent of Internet 2.0 and the 2008 financial crisis (when a lot of folks had their faith in banks shaken), some brainy computer expert types started to wonder if there might be a way to create equally perfect and trustworthy records for these gazillions of transactions, but without those fiduciary third parties, the banks. Thus was born the blockchain.

A blockchain accomplishes the same accounting task as banks. However, instead of using two private ledgers for the buyer and the seller, all transactions are recorded together on the Internet, in a single, unalterable public ledger. In the crypto universe, Bob charges you the same price for your shoes (let’s call it 100 “coins”). You use your “crypto wallet” to move 100 coins into Bob’s account, and the transaction is recorded on your crypto coins’ blockchain. A large number of computers around the world maintain and monitor the blockchain ledger, in real time, 24 hours a day. All of those computers then confirm and approve your transaction.

A few years ago, the folks at Ethereum looked at this and saw that an adaptation of the blockchain ledger technology could be used to keep track of—and certify ownership of—a digital file, such as a Tweet or a JPEG or a GIF, by attaching a unique digital certificate to its purchase/sale transaction entry. That certificate is called a token—hence the T in NFT—and if said certificate is unique, it is also non-fungible: the NF in NFT. It tells the world that you own the original version of whatever that file happens to be, even if someone else copies or steals it.

The Value Proposition

How does one determine the value of an NFT? This is where I join you in a little head-scratching. Boosters of NFTs say that they’re like unique collectible cards that anyone can see online, but only one person can claim ownership of them at any given time. The concept behind an NFT is that this scarcity—which exists, is recognized and is understandable in the physical world—will confer a similar value in the virtual world of the Internet.

Can an NFT be copied? Yes. However, the original NFT address can be traced back to the original creator, since all NFTs have an indelible record of their transaction history on the blockchain. One of the current criticisms of NFTs, however, is that unlawful copies can be difficult to detect and police.

I know. I give up, too. But let’s keep moving.

There are four principal metrics of NFTs that determine their potential market value:

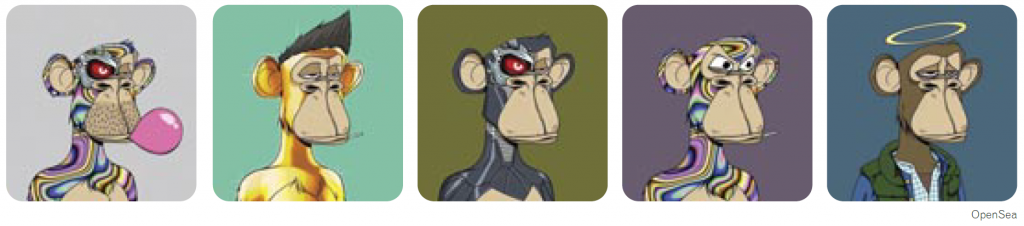

1) Primacy. Just as Bitcoin became the dominant cryptocurrency because it was the first, the first NFTs minted by certain creators and businesses tend to hold the highest perceived value. For example, Jack Dorsey’s first Tweet. You may have heard of the Bored Ape Yacht Club. It was the first “gallery” of digital art that caught the imaginations of celebrities and other people with way too much disposable income, and has since benefited from this caché, with prices for a cartoon ape bringing six- and seven-figure prices on OpenSea (more about that on the next page).

2) Scarcity. Think of a masterpiece painting. Everyone can have a copy of it and tack it up on their dorm room walls, but only one person (or museum) can hang the original. Or let’s say Madonna minted only one NFT ever—maybe a video file from her new documentary Madame X—but then tragically perished in a plane crash. Since there is only one, it might potentially become very valuable.

3) Provenance. Let’s say that Mark Wahlberg donates a leather jacket to a charity auction. It may have cost him $500 brand new, but now it’s just used clothing. Or is it? Because it’s celebrity used clothing, his fans might be willing to pay thousands for it. Now suppose that Mark wants to donate an NFT for a JPEG photo of himself and his family. Wouldn’t those same fans fight over that photo?

Gabbo T

4) Utility. Imagine if Taylor Swift sold 50 (and only 50) NFTs that granted their owners lifetime back-stage access to all of her live performances. These 50 NFTs would soar in value due to their real-world benefits. This is an example of a “smart contract,” which is an interesting quality of an NFT. Personally, I regard this as the only rational use for an NFT.

All four metrics are entirely dependent on the principle of “digital ownership.” NFTs are the digital equivalent of personal property. They reside in an owner’s crypto wallet, and for the most part can be used however and wherever the owner wants. If the “Metaverse” (uh-oh I see a third EDGE assignment coming!) takes off as the tech world believes it will, NFT “objects” will be used more and more in video games or other interactive situations where they would have monetary value.

Nuts and Bolts

www.istockphoto.com

How do you buy an NFT? Most are sold on marketplace web sites similar to eBay but specializing in NFTs, among them the aforementioned OpenSea. The vast majority are only available to be purchased using Ethereum, so you will need to own some Ether, the cryptocurrency developed by Ethereum to be just as dependable, but a little more nimble, than Bitcoin. Establishing a crypto wallet requires a degree of technical skill and, if you make a mistake, you might very well wind up losing your NFT, as well as your Ether.

Step 1: Create an account wallet on the NFT marketplace website of your choice

Step 2: Create an account wallet and purchase Ethereum on an exchange website

Step 3: Transfer your Ethereum from your exchange wallet to your marketplace wallet

Step 4: Bid in the auction for the NFT of your choice. If you win, that NFT is added to your marketplace account wallet. Where do you store your Ethereum and your shiny new NFT? The best place is on a third, offline “hardware wallet.”

Given how fast the NFT craze grew in 2021, you knew there would be some technical glitches. Some have been expensive. In one case, digital thieves were able to exploit a loophole in OpenSea’s exchange and snag an astronaut Bored Ape for $700,000 less than the asking price—and then flip it to another buyer for a quick profit.

Today there are tens of thousands of NFTs of all kinds—for visual art, music, sports videos… you name it. Since about 18 months ago, people have been buying all kinds—sometimes for boatloads of Ether. In March 2021, an NFT of a single JPEG image file sold at Christie’s auction house for $69 million worth of Ether. One month later, an NFT of Jack Dorsey’s first Tweet on March 22, 2006 (the very first Tweet) was bought for $2,915,835.47 (fun fact: it’s a prime number). An NFT of a LeBron James highlight video file sold for $208,000 just over a year ago.

It gets weirder. A 12-frame animation GIF by artist Chris Torres of a NYAN Cat with a frosted Pop Tart body flying through outer space, trailing rainbows behind it, sold for $600,000. Thousands of ape pictures created by Bored Ape Yacht Club (BAYC) are still generating hundreds of millions of dollars and are owned by some of the world’s most recognizable celebrities—including Snoop Dogg and Paris Hilton.

If you’re asking yourself just now: How are there so many idiotic NFT things that you’ve never heard of raking in so much lucre? Well, I’m with you. As a rule, anything two mental giants like Paris Hilton and Snoop Dogg are fascinated by, I turn from and run. Finally, here are my personal conclusions and, fair warning, they’re not favorable…

NFTs have all the earmarks of a scam IMHO (in my humble opinion)—a speculative bubble rife with ethical and financial rabbit holes. A “greater fool” game, if you will. It reminds me of what happened in the online retro games market not too long ago, when a bunch of dishonest guys bought each other’s collections to increase their perceived value—a practice known as “wash trading.”

NFTs depend on creating perceived value by fabricating scarcity that is normally found in physical objects. My question is, why restrict an infinitely reproducible digital file’s reproducibility unless you plan to sell it? Or, more precisely, resell it? You don’t buy an NFT to hang on your wall. You really can’t even keep other people from looking at it, if they want. You hope that its perceived value increases so you can dump it and make a profit.

If that sounds like stocks, bonds, commodities futures, etc. that are also speculative, it’s meant to. But trading in NFTs reminds me more of the old 1960s Milton Bradley party game, Time Bomb, where someone wound up the ticking egg-timer fuse on an explosive device and you’d pass it around a circle until it went off in some poor kid’s hands. It’s gambling, only with worse odds—like sitting down to a rigged poker game where the dealer and the other players are all working for the house.

So What Is an NFT, Really?

www.istockphoto.com

It is not much more than a gilded receipt for a digital luxury item. An original physical artwork is distinct from a reproduction; if you value that artwork, then there is genuine subjective benefit in owning it. But with digital art, reproductions are inherently perfect copies, so “original” means nothing. Anyone other than the owner can access and copy an NFT. The person copying it just can’t own it. In some cases, an NFT buyer doesn’t even get a traditional copyright (the buyer of the NYAN Cat, for example, did not receive the right to reproduce or merchandise the image from the artist). Meanwhile, many artists excited by NFTs’ potential as a revenue stream watched in dismay as their artwork was turned into unauthorized NFTs and sold without their knowledge or permission, in a market sorely lacking in effective oversight. That being said, among the most ardent supporters of NFTs as “the next generation of art” is Time magazine and its Timepieces Community, which features more than 20,000 NFTs.

NFTs might serve a use as a digital representation of a physical object, like a concert ticket—and are potentially great vehicles for money laundering. Otherwise, in and of themselves, I feel they are pointless.

NFT? No Freaking Thanks.

Editor’s Note: Luke Sacher is a documentary filmmaker who has written extensively on technology and popular culture for EDGE. Since he was assigned this story late in 2021, sales of NFTs have fallen more than 70%.